- About

- Our markets

- Our Solutions

- Our products

BNA Bank launches Digi Pay, its mobile payment solution

Mobile Payment in Tunisia: the political will and the synergy between the actors, key factors of success

Podcast on Express FM of Thursday 11th June 2020 with Mr Moez EL GHALI CEO of MS Solutions

Moez EL GHALI, also president of the CJD (Centre for Young Business Leaders) spoke of what we have experienced since the beginning of the year 2020 with Covid-19, saying that it's "a crisis that has revealed FAILURES and the need to REFORM as a matter of urgency". After an initial old-fashioned distribution, the social aid was then distributed via mobile phones thanks to a project led and offered by MS Solutions.

"We're still moving forward," he says. In fact we are making considerable progress with MS Solutions since the BNA's DIGIPAY mobile payment application (Mobile Payment) has enabled a customer to pay at a merchant whose bank is the Banque de l'Habitat. That's what's called interoperability in the jargon. In other words MS Solutions has developed a platform while creating an ecosystem between banks and third party payment institutions such as CNSS, STEG and STA (Société Tunisie Autoroutes). Thus, any citizen, whether or not they have a bank account, will be able to download the Digital Wallet application onto their mobile phone to deposit money and pay with it, for example at a petrol station or in a shop.

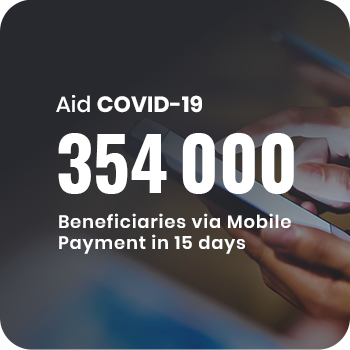

Finally, Moez EL GHALI specifies that the technical aspect was ensured by MS Solutions but that the monitoring and the follow-up will have to be ensured by the authorities as it was the case for the social aids during Covid-19. Indeed, the synergy of the efforts of the central bank, the ministry of finance, the post office, the banks, the SNT (Société National de Transport) and the CNI (Centre National de l'Informatique) made it possible to achieve in 2 months what under normal circumstances would have been achieved in 4 to 5 years. As a result, 354 000 people entitled to Covid-19 gouvernment financial aid were able to apply for it from their mobile phones, receive it on their phones and from their phones withdraw their money at any withdrawal point or post office or bank branch.

This is fully interoperable, in other words, for both unbanked citizens and banked people, regardless of their bank.

To conclude, and as Moez EL GHALI points out, "what would make a citizen use his phone to pay when he has cash in his pocket? " The answer is when it would be cheaper, and this is where the political will and synergy of the different actors is needed.