SoftPOS in Banking Environments

Modern Acceptance. Full Compliance.

Contactless payments are now formalizing software-based acceptance under PCI and major card network security frameworks. Software-defined acceptance is no longer experimental. It is becoming embedded within the regulated payments landscape.

Yet for banks operating under strict supervisory, scheme, and audit requirements, the adoption question is not about capability, it is about control.

The structural challenge for Banks

Expanding acceptance has traditionally relied on scaling physical terminal estates, an approach that remains essential for high-volume retail, fixed-location merchants, and complex payment environments. Managing these estates requires structured deployment, lifecycle coordination, and operational oversight.

SoftPOS introduces an additional form factor within this landscape. In regulated banking environments, however, any new acceptance endpoint must operate under the same pillars.

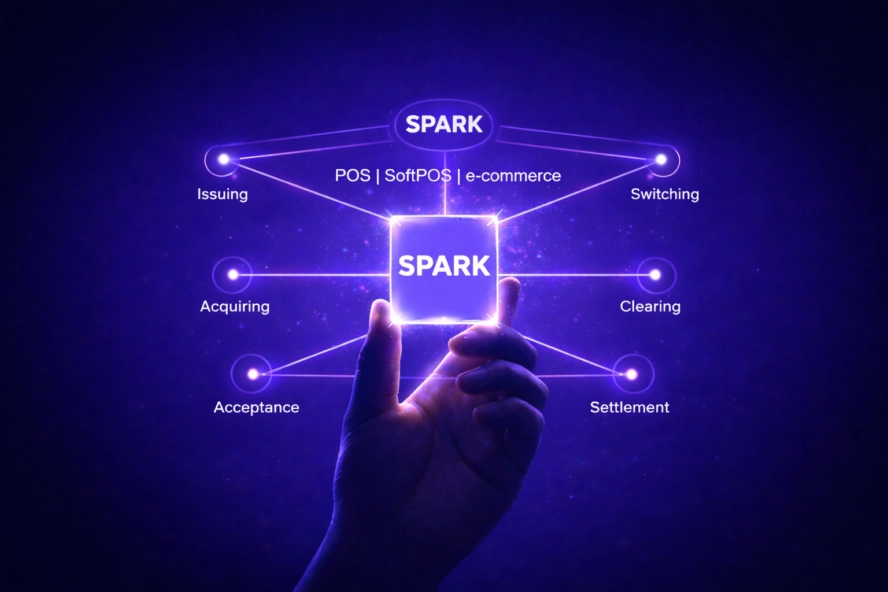

The strategic issue is therefore not whether to adopt SoftPOS, nor to replace existing infrastructure, but how to embed new acceptance form factors within the acquiring perimeter while preserving operational discipline across all channels.

If deployed outside the following Acquiring core, software-based Acceptance can introduce fragmentation, parallel reconciliation layers, inconsistent controls, and expanded regulatory exposure:

- Governance standards

- Authorization integrity

- Dispute readiness

- Transaction traceability

- Risk and fraud oversight

- Settlement and reconciliation consistency

Beyond efficiency: expanding and optimizing the Acceptance Network

In many markets, micro-merchants, informal businesses, and mobile professionals remain underserved by traditional deployment models, not because physical POS lacks value, but because merchant economics and mobility requirements vary significantly.

Software-defined acceptance lowers structural barriers to entry while allowing banks to optimize their acceptance mix.

When embedded within the acquiring architecture, SoftPOS enables institutions to:

- Broaden coverage across underserved merchant segments

- Accelerate onboarding cycles

- Increase digital transaction penetration

- Support national financial inclusion strategies

- Optimize allocation of physical POS estates by merchant profile and throughput

In this context, SoftPOS becomes both a commercial expansion lever and a strategic inclusion enabler if it operates within a unified and regulated framework.

Orchestrating POS and SoftPOS within a unified architecture

Physical POS terminals remain essential for high-volume retail, multi-lane environments, and complex peripheral integrations. They anchor processing capacity, stability, and performance.

SoftPOS introduces flexibility, extending acceptance where mobility and rapid deployment are required.

For regulated institutions, the objective is not substitution. It is orchestration. Both forms of Acceptance must operate:

- Within the same acquiring architecture

- Under unified risk controls

- With consolidated reconciliation and reporting

- Inside a controlled PCI and certification perimeter

The modern acceptance strategy is therefore platform-based by design, combining physical and software-defined endpoints within a single governance framework.

- Embedding new endpoints directly into switching and authorization layers

- Maintaining end-to-end encryption and HSM-backed key management

- Preserving centralized monitoring and auditability

- Ensuring consistent settlement and dispute processes across all channels

When these conditions are met, SoftPOS strengthens rather than fragments the acquiring ecosystem.

A unified Acceptance strategy

The next phase of Acquiring modernization is not about replacing terminals. It is about extending the Acceptance perimeter, securely, compliantly, and strategically.

By integrating SoftPOS alongside traditional POS within a unified platform architecture, banks can:

- Expand reach across underserved segments & Support financial inclusion

- Optimize deployment models

- Preserve regulatory control and operational integrity

Across multiple regulated markets, MS Solutions Group clients have been early adopters of SoftPOS, they reported:

- Accelerated merchant activation

- Expanded acceptance coverage in underserved segments

- Optimized allocation of physical POS estates

- Improved operational visibility across acceptance channels

This model enables banks to expand and modernize their acceptance networks while preserving architectural coherence across the full payment value chain.